While 2025 offers some hope mortgage rates will move lower, that’s still very much up in the air.

There are renewed worries that inflation could reignite, pushing rates higher in the New Year.

Especially as we welcome a new president who has promised to introduce some inflationary policies, such as widespread tariffs.

This not only affects prospective home buyers grappling with strained affordability, but also existing homeowners looking to refinance.

After all, millions still managed to take out mortgages when rates were in the 7-8% range, and they’re quite rightfully looking for relief.

How Can We Make the Decision to Refinance a Little Easier?

One thing I want to point out first is that there’s no single refinance rule of thumb. Sure, I wish there was.

It’d be great if you could make one blanket statement to help homeowners decide if they could benefit or not. But this just isn’t the case.

There are far too many variables involved with mortgages and real estate to do that. But we can at least pluck out some tips to make the decision easier.

Today, I’m focusing on rate and term refinances, which allow borrowers to trade in their old loan for a new one with a lower interest rate and new term.

These are pretty much the only game in town right now because cash out refinances don’t make much sense given rates aren’t all that attractive.

Anyway, one thing to consider when making a refinance decision is the size of your outstanding loan balance.

Simply put, a larger loan amount makes a refinance pencil much more easily because it results in greater savings.

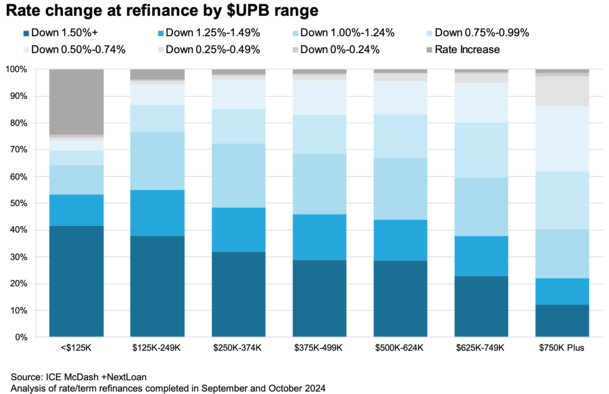

Homeowners with Bigger Loans Require Less Rate Movement to Refinance

The most recent monthly Mortgage Monitor from ICE does a great job illustrating how loan amounts affect refinance decisions.

They noted that for most borrowers with loan balances below $250,000, a rate reduction of at least 125 basis points (1.25%) was required for them to move forward and apply.

In other words, if their rate was 7.75%, it’d need to be at least 6.5% to consider the refinance worth it. Obviously this can be a pretty big ask as that’s a wide gap between rates.

Fortunately, mortgage rates did fall to those levels in August and September, before bouncing higher after the Fed cut its own rate.

Anyway, on the other end of the spectrum were the folks with loan amounts of at least $750,000.

For this cohort, they could act on a mortgage refinance with far less incentive. ICE found that roughly 40% of them lowered their rates by just 75 basis points or less.

From say 7.25% to 6.5%. And another 12% of these larger loan borrowers felt that refinancing was worth it for a rate less than 50 bps lower.

In other words, going from 7% to 6.5%. Doesn’t seem like a lot does it?

Lastly, those with really small loan amounts, think less than $125,000, we’re actually okay with raising their mortgage rate, with about 25% opting for this.

Why? Well, they probably went with a cash out refinance because they needed money. And since their loan amount was small, there was less incentive to hang on to the old loan.

This runs counter to those with bigger loans at 2-4% rates who are experiencing mortgage rate lock-in.

Let’s Do the Math to Find Out Why Loan Amounts Matter on Your Refinance

| $250k loan amount | $750k loan amount | |

| Old mortgage rate | 7.75% | 7.25% |

| Old payment | $1,791.03 | $5,116.32 |

| New mortgage rate | 6.50% | 6.50% |

| New payment | $1,580.17 | $4,740.51 |

| Difference | $211 | $376 |

Taking the two loan scenarios I threw out above, we’ve got a borrower with a $250,000 loan amount and a 7.75% mortgage rate.

They see it’s possible to refinance down to 6.50%, which is a huge move rate-wise. But how much does it actually save them per month?

Only about $211 per month. Not an incidental amount, but it does illustrate why a big rate move was required to make any associated or upfront costs worth it.

Remember, you want to keep the loan long enough to justify the closing costs involved in the transaction.

Then we have our $750,000 borrower with a 7.25% rate that is refinanced down to 6.50%.

This results in savings that are nearly double ($376) versus the other borrower, despite a much smaller improvement in rate.

The caveat here is the borrower with the smaller loan amount might view $200 is savings as equally or more valuable than the borrower with the larger loan amount who saved nearly $400.

But if someone tries to tell you that rates need to fall by X amount for your refinance to be worth it, ignore them.

Instead, take the time to do the actual math to see exactly how much you stand to save. Or perhaps not save!

There are no shortcuts if you want to save money on your mortgage. However, if you put in the time the ROI can be pretty incredible.

(photo: The Harry Manback)

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 18 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on Twitter for hot takes.

{kind=link}