14 housing trends that defined the year, including record house prices, a mortgage rate rollercoaster, and a sales sea-saw

The 2024 housing market in many ways mirrored 2023: too few homes on the market, and not enough buyers willing to face high prices and mortgage rates. This pushed house prices higher and kept affordability historically low – remarkable, given that 2023 ended as the least affordable year for homebuying on record. Nearly 40% of renters thought they’d never own a home.

The market was so difficult that the median homebuying age jumped to a record 56 years old – seven years older than 2023. A greater proportion of homebuyers continued to get priced out.

Many homebuyers sat out the year on the sidelines, waiting for affordability to improve. Others got tired of waiting and decided to take the leap, even with the market headwinds. The presidential election also injected more volatility and unpredictability.

However, there were some key improvements, including more housing inventory, declining inflation, and improved renter affordability.

Below are trends, data points, and visuals that defined the 2024 housing market.

All data was aggregated from January through November 2024 unless otherwise stated. Data came from Redfin, Rent., the U.S. Census Bureau, FRED, NAR, and/or public records. For questions about metrics, read our metrics definitions page.

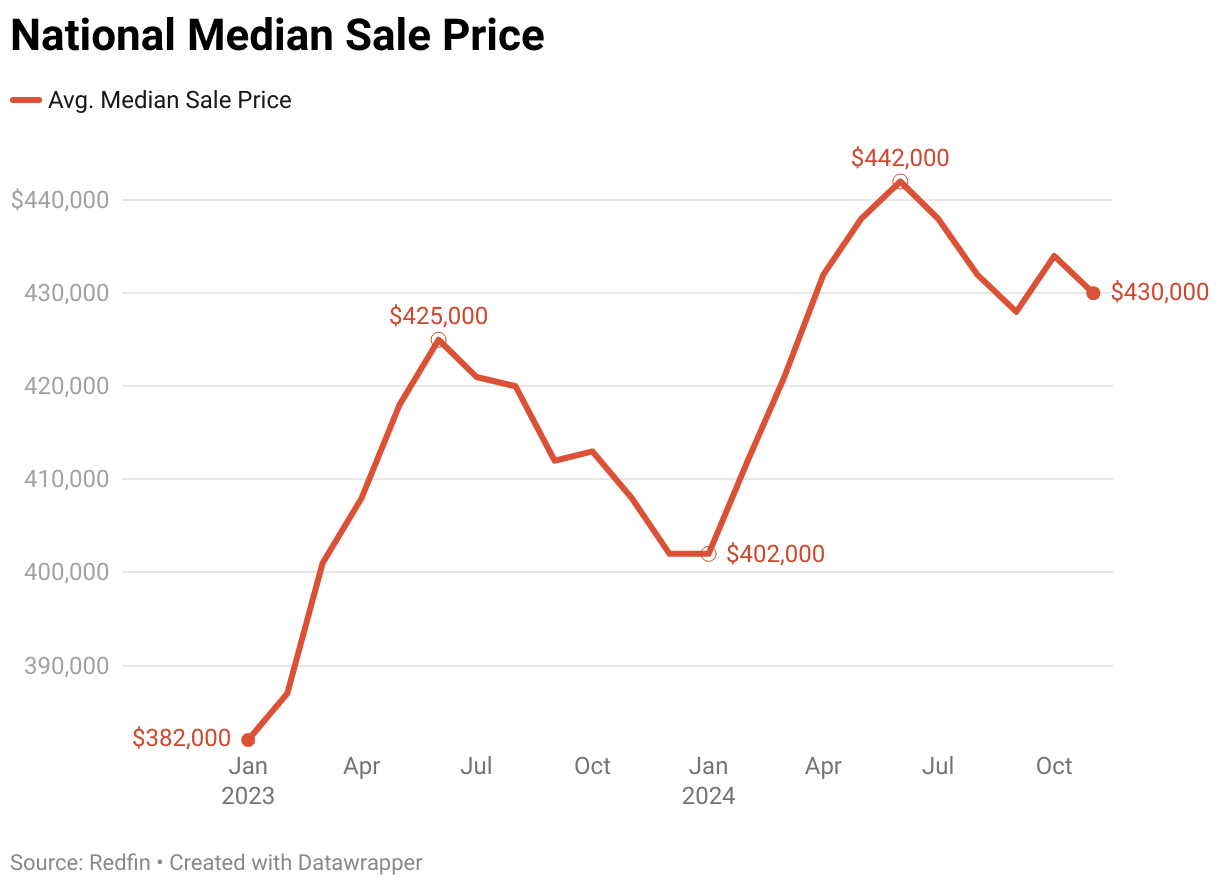

1. Home prices reached consecutive all-time highs

The U.S. median sale price reached an all-time high in July when it hit $442,000, one month after June recorded a high of $438,000. Both eclipsed 2022’s record of $432,000. House prices hit record highs for nine straight weeks.

When averaging for the entire year, 2024’s median sale price of $428,200 far surpassed any previous year in history, beating last year’s by $20,000.

“Supply and demand played starring roles again this year,” said Daryl Fairweather, Redfin Chief Economist. “The combination of low supply and lackluster demand gave buyers the reality of a hot market, even though few homes changed hands. This unusual trend helped push prices steadily higher throughout the year, which was bad news for everyone except homesellers looking to downsize or rent.”

Low-income residents were hit especially hard. Nearly a quarter who made less than $50,000 had to skip meals to afford payments.

2. San Jose was the most expensive metro area for homebuyers in 2024

Beating out San Francisco, San Jose became the most expensive metropolitan area for homebuyers in the country in 2024. The average monthly median sale price in San Jose was $1,566,100, up 8.5% ($133,120) from last year. Otherwise, the top ten most expensive markets were unchanged from 2023.

House prices generally rose across the board, with only Austin and San Antonio posting year-over-year decreases. Housing affordability became an even larger crisis this year, especially among lower-income groups, and was a major issue for voters in the presidential election.

- The top six most expensive metros were all in California.

- Anaheim saw the largest year-over-year price increase in the country, rising 12.5%.

3. Detroit was the least expensive metro area for homebuyers in 2024

The average monthly median sale price for a home in Detroit was $190,865, up 8.5% ($16,220) from 2023. Prices have risen dramatically since the pandemic, as buyers searching for affordability fought for a limited supply. Many of the most affordable metros were top choices for relocating homebuyers early in the year and have seen large price growth since the pandemic.

- All but one of the most affordable metros saw substantial (>5%) year-over-year gains.

- Nine of the ten least expensive metros were all located in the Rust Belt, continuing last year’s trend.

Austin (-2.2%) and San Antonio (-1.8%) posted the only year-over-year drops in the nation. Both also saw the greatest improvements in affordability when factoring in wage growth.

4. Home sales turned positive for the first time in years

4.62 million U.S. homes sold through November 2024, a slight increase from last year but far below the 5.62 million sold in 2022. On average, 423,100 homes sold every month this year, beating last year’s 417,020.

Year-over-year home sales were negative every month in 2024 before turning positive in September – the first time in over three years. Sales posted stronger increases of 4.8% in October and 7.2% in November, which was a promising upward trend leading into 2025.

Sales likely turned positive because mortgage rates dipped significantly in August and September. And pending sales, a 1-2 month leading indicator of closed home sales, showed strength later in the year, too.

Home sales likely increased because more buyers accepted that mortgage rates will hover between 6-7% for now.

- May saw the fewest home sales, at just 412,150. There have only been two months since 2012 with fewer sales.

- To close out the year, home sales posted major increases in expensive West Coast markets, likely because a shortage of homes intensified competition.

- While sales rose overall, they often fell when mortgage rates spiked. In October, when rates rose from 6.2% to 7%, roughly 53,000 home purchases were cancelled – the highest share in a year.

- Two hurricanes and an insurance crisis helped cause Florida metros to see the biggest drops in home sales: West Palm Beach (-9.2%), Fort Lauderdale (-7.9%), Miami (-4.6%), Tampa (-3.9%), and Jacksonville (-3.9%). On the other hand, the drop in sales helped boost supply.

5. Mortgage rates went on a rollercoaster ride

“Once again, mortgage rates dominated the market this year,” continued Fairweather. “Rates hovered between 6.5% and 7.5%, which scared off many buyers and pushed sellers to hold onto pandemic-era rates.”

Rates were stubborn, too. “Even though inflation dropped close to the Fed’s 2% target and we saw three interest rate cuts, uncertainty over the election and strength of the economy kept rates elevated,” she added.

Demonstrating how volatile rates were, a weak jobs report in August led investors to push mortgage rates down to 6.3%, which prompted a surge in buyer activity. Rates fell further in September, but then quickly rose with the prospect of a stronger-than-expected economy. We don’t expect mortgage rates to change significantly in 2025.

Buyers who are wary of an expensive market should understand that historically, rates are relatively average. “If you’re ready to buy a home, now is the time to talk with an agent, get prequalified for a mortgage, and start your home search,” advised April Janas, Senior Loan Officer with Bay Equity, a Redfin company. “Many markets cater to buyers right now, with more options, less competition, and favorable terms. And if rates do fall in 2025, there are ways to take advantage, including refinancing your mortgage.”

- The Fed is expected to cut interest rates only twice next year, less than previously forecast.

- However, there is a lot of economic uncertainty due to President-Elect Trump’s potentially inflationary policy proposals, including tariffs, tax cuts, and deportations.

6. Inflation finally cooled down, but the future is uncertain

The Fed’s aggressive rate hikes from 2022 to 2023 finally helped bring down inflation from record highs. In November this year, the inflation rate sat at 2.7%, just above the Fed’s target but relatively healthy historically. The Fed responded by issuing three consecutive rate cuts.

However, experts are wary that inflation could increase again next year, especially if Trump’s policies pan out. The Fed’s updated projections for 2025 suggest that they plan to act with more caution and cut rates more slowly.

As interest rates hovered around 0.5% for the entirety of the pandemic, inflation took off due to supply crunches and increased consumer demand. The Fed responded by raising the benchmark interest rate 11 times over the course of a year to combat inflation and cool the economy.

7. Rents held steady

The median U.S. asking rent reached a high of $1,649 this year, similar to last year and a continued reprieve from the pandemic-era rollercoaster. Rents stayed mostly flat all year and dipped leading into 2025. The median asking rent across all months through November averaged $1,629 – just $8 more than last year.

But when paired with slowly rising wages, rentals actually became slightly more affordable. Rents for college graduates and teachers saw notable improvements.

The calmer market was driven by a surge of new apartments completed this year after the construction boom in 2021-2022. Now, supply is outpacing demand, and new units are renting more slowly. Apartment construction has since slowed.

Rents fell fastest in the Sun Belt and some coastal metros, which built the most apartments during the pandemic. Florida and Texas saw large drops this year. The opposite was true in Rust Belt and East Coast metros, which didn’t build as much and were then faced with a supply shortage.

Importantly, though, rents have remained historically unaffordable since the pandemic, skyrocketing by 19% from 2019. A record half of all renters spent more than a third of their income on rent this year, and 22% spent their entire paycheck. Incomes have lagged behind rents for years, impacting low-income renters the hardest. This lack of affordability, and the likelihood of facing higher rents in a new apartment, has led many renters to stay put.

8. New construction slowed down

The U.S. saw an average of 1.35 million new homes started monthly in 2024, down from 1.42 million in 2023 and well below 2022’s 1.55 million. New single-family home construction (excluding rentals) fared similarly to last year, peaking at 1.13 million in February.

We expect new construction to rise next year, though. “This should have a positive effect on supply in the next few years,” noted Chen Zhao, Redfin Senior Economics Manager. “New construction has lagged since the Great Recession but has been slowly recovering, peaking just after the pandemic. Construction dipped this year, but builder confidence has improved heading into 2025.”

However, even with post-pandemic improvements, the country is still experiencing a historic shortage of affordable housing. New construction trails well behind demand, and the U.S. has a housing shortage of between 2-6 million units.

Homebuilders have backed off since the pandemic-driven building boom, with high mortgage and interest rates hampering buyer demand and pushing up development costs. Many builders are now focused on selling the homes they have. This helps to explain why just 28% of houses for sale in September were newly built this year – the lowest share in 3 years.

- California, Oregon, and Utah are among states that fall the farthest short of projected housing needs.

- Housing completions fared slightly better than starts, with an annualized rate of 1,601,000 in November – a 0.2% year-over-year decrease.

- Permits to build single-family homes increased this year, but are still well below post-pandemic highs.

Data was seasonally adjusted through October 2024.

9. Housing inventory posted major gains

On average, 1.19 million homes were listed for sale or pending every month through November in 2024, up a massive 15.8% from last year. Monthly inventory peaked at 1.21 million homes in October.

Inventory rose for a few reasons: more sellers decided to test the market; homes sat on the market for longer; and new housing completions continued to steadily rise.

Active listings, a measure of all homes on the market, have steadily increased since mid-2023, hitting a high of 1.73 million in November. Active listings and pending sales make up the total housing inventory.

Even though inventory has begun recovering from chronically low supply and the pandemic homebuying craze, it still sits below the historical normal. There aren’t enough affordable homes on the market.

Inventory is seasonally adjusted and calculated in rolling 90-day periods, e.g., January 2024 data is the three-month period from November 1, 2023, through January 31, 2024. Redfin inventory records date back to 2012.

10. New listings continued climbing

In line with inventory, new listings posted major gains this year. An average of 544,000 homes were newly listed for sale every month in 2024, up 9% from 2023’s record low. New listings have slowly improved over the past two years.

The rise in listings took a while to translate to sales, though, as high housing costs priced many buyers out of the market. It wasn’t until later in the year that market activity really picked up following Fed rate cuts and rises in affordability.

New listings are seasonally adjusted and calculated in rolling 90-day periods, e.g., January 2024 data is the three-month period from November 1, 2023, through January 31, 2024. Redfin listings records date back to 2012.

11. Months of supply continued its steady recovery

While inventory measures the number of homes currently available for sale, months of supply measures the amount of time it would take those homes to sell. Four to five months of housing supply is considered a balanced market, with more indicating a buyer’s market and fewer indicating a seller’s market.

The average stock of housing supply across every month in 2023 was 2.8 months, up from 2.5 months in 2023. The market continued to lean towards sellers, but swung closer to buyers in certain markets, especially expensive metros with limited demand. More affordable metros often saw the opposite trend.

Even though supply rose further in 2024, many buyers had to fight for every home; through the first eight months of the year, just 2.5% of the nation’s homes changed hands – the lowest share since at least the 1990s. The pandemic homebuying boom depleted supply, further hampered by a spike in investor purchases, which has only started to recover.

“Supply has slowly pulled itself out of its pandemic-infused slide and continued to gain ground this year,” added Fairweather. “However, it’s still far from a balanced market. Buyers and sellers should talk with an agent to determine how best to navigate their local market.”

- Supply peaked at 3.3 months in January and fared better than last year during the homebuying season.

Supply is seasonally adjusted calculated in rolling 90-day periods, e.g., January 2024 data is the three-month period from November 1, 2023, through January 31, 2024. Redfin supply records date back to 2012.

12. The typical home took more than a month to sell

Homes spent an average of 39 days on the market in 2024 – a day longer than 2023. Home sales continued their major slowdown from the record-breaking pace seen in 2021-2022, largely because affordability was so strained.

This slowdown was especially visible in September, when half of all homes listings had sat on the market for more than 60 days. The trend continued into December. That was up from 43.2% in 2023. Previously in May, more than three-fifths had been on the market for 30 days, up from 60% in 2023.

However, time-on-market varied widely by metro; homes in affordable metros often sold much more quickly than homes in expensive metros. For example, in May, the typical home in Buffalo sold in just 8 days, compared to 45 days in Austin. Some pricier West Coast markets, like San Jose, saw jumps in sales to close out the year, too.

As homebuying affordability worsened, people just wanted a home they could afford.

- Many historically popular and affordable Sun Belt cities, like Jacksonville, saw demand skyrocket during the pandemic. Now, they’re cooling off and homes are taking longer to sell.

- May and June were the busiest months of the year, with homes spending 32 days on the market.

- Even though they’re slowing down, homes still sell historically quickly on average.

13. Nearly 31% of homes were purchased with cash in 2024

30.8% of homes were purchased entirely with cash in 2024 – down from 32% last year but still historically elevated.

All-cash sales generally follow the same trend as the rise and fall of mortgage rates. When rates move down, the percentage of all-cash sales moves down; when rates go up, all cash-sales go up. So, as mortgage rates skyrocketed in 2022, all-cash purchases followed suit. They have remained elevated since, but are falling.

Luxury buyers and investors were much more likely to pay in cash.

“By paying all cash, affluent buyers can bypass interest rates altogether and secure a better deal,” continued Zhao. “While these are great benefits, they can contribute to inequality between people who own homes and people who don’t, especially since investors tend to gravitate toward lower-priced homes.”

- All-cash sales slowly fell throughout the year from a February peak, as rates dipped and homebuying activity returned.

- Popular, inexpensive metros saw the highest share of cash purchases.

- Many of the most expensive metros saw the lowest share of all-cash purchases, including San Diego (22.1%), Virginia Beach (21.9%), and Seattle (20.7%).

14. Investor purchases rebounded following two years of decline

Real estate investor purchases rose for the first time since 2022 this year, when they climbed 0.5% in March. Activity increased as the year went on and ended at pre-pandemic levels – impressive, given the wild swings the industry has seen. Investor purchases surged as much as 144% year over year in 2021, then dropped as much as 47% last year.

When averaging over the entire year, investor purchases slightly increased from 2023, hovering just above 17%.

Investors generally buy homes to either sell or lease and capitalize on low construction costs and high demand. When costs are high and demand is low, investors usually slow down purchases.

Since mid-2022, investor market share has posted negative year-over-year growth every quarter, dropping from a record 20% in 2022 to 16% in 2023. Now that house prices are hitting new highs and the shock of high mortgage rates is in the rearview mirror, investors are reentering a more appealing market.

- Investors made more money compared to a year ago. In March, the typical home sold by an investor went for 55% more than they bought it for.

- Investors backed out of Sun Belt metros the fastest, with Fort Lauderdale (-13.1%) and Miami (-10.6%) seeing among the largest drops in purchases.

- Even though investor market share has declined since the pandemic, it’s still historically very high.

- Multi-family homes continued to be the most popular among investors, with condos coming in second.

Looking forward

The 2024 housing market was tough for many homeowners and renters, but what does Redfin predict for 2025? Read our 2025 Housing Market Predictions to learn more.

{kind=link}