When the housing market crashed in the early 2000s, new mortgage rules emerged to prevent a similar crisis in the future.

The Dodd-Frank Act gave us both the Ability-to-Repay Rule and the Qualified Mortgage Rule (ATR/QM Rule).

ATR requires creditors “to make a reasonable, good faith determination of a consumer’s ability to repay a residential mortgage loan according to its terms.”

While the QM rule affords lenders “certain protections from liability” if they originate loans that meet that definition.

If lenders make loans that don’t include risky features like interest-only, negative amortization, or balloon payments, they receive certain protections if the loans happen to go bad.

This led to most mortgages complying with the QM rule, and so-called non-QM loans with those outlawed features becoming much more fringe.

Another common feature in the early 2000s mortgage market that wasn’t outlawed, but became more restricted, was the prepayment penalty.

Given prepayment risk today, perhaps it could be reintroduced responsibly as an option to save homeowners money.

A Lot of Mortgages Used to Have Prepayment Penalties

In the early 2000s, it was very common to see a prepayment penalty attached to a home loan.

As the name suggests, homeowners were penalized if they paid off their loans ahead of schedule.

In the case of a hard prepay, they couldn’t refinance the mortgage or even sell the property during a certain timeframe, typically three years.

In the case of a soft prepay, they couldn’t refinance, but could openly sell whenever they wished without penalty.

This protected lenders from an early payoff, and ostensibly allowed them to offer a slightly lower mortgage rate to the consumer.

After all, there were some assurances that the borrower would likely keep the loan for a minimum period of time to avoid paying the penalty.

Speaking of, the penalty was often pretty steep, such as 80% of six months interest.

For example, a $400,000 loan amount with a 4.5% rate would result in about $9,000 in interest in six months, so 80% of that would be $7,200.

To avoid this steep penalty, homeowners would likely hang on to the loans until they were permitted to refinance/sell without incurring the charge.

The problem was prepays were often attached to adjustable-rate mortgages, some that adjusted as soon as six months after origination.

So you’d have a situation where a homeowner’s mortgage rate reset much higher and they were essentially stuck in the loan.

Long story short, lenders abused the prepayment penalty and made it a non-starter post-mortgage crisis.

New Rules for Prepayment Penalties

Today, it’s still possible for banks and mortgage lenders to attach prepayment penalties to mortgages, but there are strict rules in place.

As such, most lenders don’t bother applying them. First off, the loans must be Qualified Mortgages (QMs). So no risky features are permitted.

In addition, the loans must also be fixed-rate mortgages (no ARMs allowed) and they can’t be higher-priced loans (1.5 percentage points or more than the Average Prime Offer Rate).

The new rules also limit prepays to the first three years of the loan, and limits the fee to two percent of the outstanding balance prepaid during the first two years.

Or one percent of the outstanding balance prepaid during the third year of the loan.

Finally, the lender must also present the borrower with an alternative loan that doesn’t have a prepayment penalty so they can compare their options.

After all, if the difference were minimal, a consumer might not want that prepay attached to their loan to ensure maximum flexibility.

Simply put, this laundry list of rules has basically made prepayment penalties a thing of the past.

But now that mortgage rates have surged from their record lows, and could pull back a decent amount, an argument could be made to bring them back, in a responsible manner.

Could a Prepayment Penalty Save Borrowers Money Today?

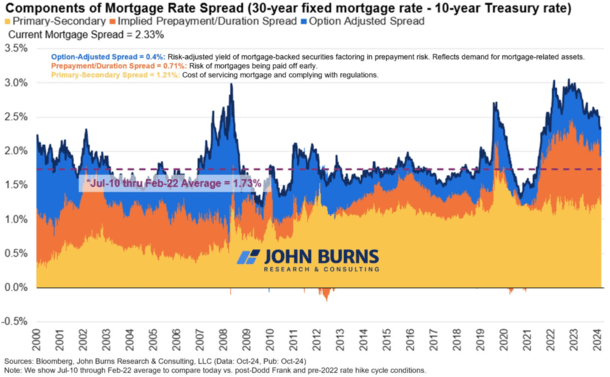

Lately, mortgage rate spreads have been a big talking point because they’ve widened considerably.

Historically, they’ve hovered around 170 basis points above the 10-year bond yield. So if you wanted to track mortgage rates, you’d add the current 10-year yield plus 1.70%.

For example, today’s yield of around 4.20 added to 1.70% would equate to a 30-year fixed around 6%.

But because of recent volatility and uncertainty in the mortgage world, spreads are nearly 100 basis points (bps) higher.

In other words, that 6% rate might be closer to 7%, to account for things like mortgages being paid off early.

A lot of that comes down to prepayment risk, as seen in the chart above from Rick Palacios Jr., Director of Research at John Burns Consulting.

Long story short, a lot of homeowners (and lenders and MBS investors) expect rates to come down, despite being relatively high at the moment.

This means the mortgages originated today won’t last long and paying a premium for them doesn’t make sense if they get paid off months later.

To alleviate this concern, lenders could reintroduce prepayment penalties and lower their mortgage rates in the process. Perhaps that rate could be 6.5% instead of 7%.

In the end, a borrower would receive a lower interest rate and that would also reduce the likelihood of early repayment.

Both because of the penalty imposed and because they’d have a lower interest rate, making a refinance less likely unless rates dropped even further.

Of course, they’d need to be implemented responsibly, and perhaps only offered for the first year of the loan, maybe two, to avoid becoming traps for homeowners again.

But this could be one way to give lenders and MBS investors some assurances and borrowers a slightly better rate.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 18 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on Twitter for hot takes.

{kind=link}