Anyone who works in the industry probably saw this coming. But those who don’t might be left scratching their head.

Yesterday, the Fed finally pivoted and cut its own fed funds rate, yet mortgage rates went up. Why does this always seem to happen?

Shouldn’t good news on the interest rate front push rates lower across the board? Seems perfectly logical until you dig into the details.

There are two main reasons why mortgage rates often defy the Fed’s own move.

One is that the Fed’s policy is often fairly telegraphed and not a surprise, and the other is that the data is typically baked in already.

The Fed Simply Follows the Economic Data

First things first, the Federal Reserve is simply making monetary policy decisions (hike, cut, nothing) based on the economic data in front of them.

So their FOMC statement and accompanying interest rate decision generally don’t come as much of a surprise.

Yesterday, there was a little more uncertainty than normal, with both a 25-basis point and 50-basis point cut a possibility.

The Fed opted to go with a 50-bps cut, which had been the favorite with a ~60%+ likelihood per CME FedWatch.

In other words, the Fed did what the market expected, as they often do. The reason the Fed does what the market expects is because they base their decisions on publicly available data.

And the data is somewhat old by the time the Fed makes its announcement. That removes much of the element of surprise.

However, what can move the bond market after the FOMC interest rate decision is the press conference with the Federal Reserve chairman Jerome Powell.

He explained that they took the step of making a 50-bps cut because they had patiently waited for inflation to come down, and were now comfortable to make a “strong move.”

The bigger cut allows them to (hopefully) avoid a big increase in unemployment while also preventing a return to high inflation.

But he added that there shouldn’t be an expectation that 50-bps cuts are the new normal. The decisions will still be made meeting-by-meeting.

So no real surprises here and not enough new information for mortgage rates to continue falling.

Mortgage Lenders Have Already Dropped Rates a Ton Leading Up to the Fed Rate Decision

The other relevant piece here is that mortgage lenders were already aggressively lowering mortgage rates heading into the Fed meeting.

If you look at the 30-year fixed, it had already fallen nearly 150 basis points (1.50%) since the end of April.

In other words, bonds and mortgage-backed securities (MBS) were making big moves based on the data and the expected Fed pivot for months now.

A lot of the price improvement, if not nearly all, was priced in before Fed day. It’s kind of a “sell the news” situation.

You know something is coming so you buy bonds or MBS and once the news actually hits, it could be time to sell off a bit.

In this case, it’s just an expected bounce in the opposite direction as everyone digests the widely-anticipated Fed decision.

To put it another way, mortgage lenders tend to price their rates defensively ahead of an FOMC interest rate decision, so often times there’s a bit of a relief rally after a hike.

Just keep in mind this is but one day, and mortgage rates may develop a longer-term trajectory based on what’s going on with the Fed and underlying economic data.

But the best way to track mortgage rates is by watching the 10-year bond yield and/or MBS prices.

Since yesterday, the 10-year yield has already ticked up about 10 basis points and MBS prices have fallen a bit.

No major movement, but perhaps a disappointment for those who thought mortgage rates would fall further after the Fed cut rates.

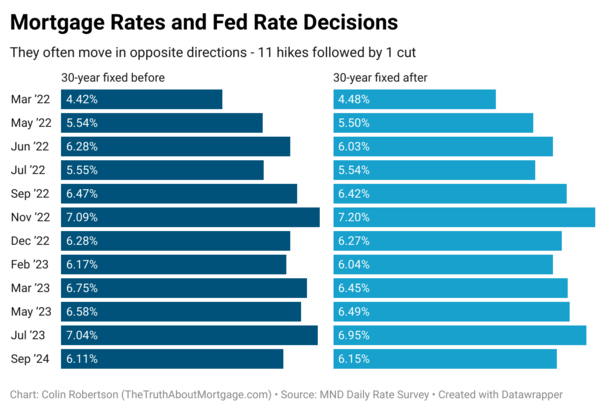

Mortgage Rates Tend to Defy the Fed

September 18th, 2024: Rate cut, mortgage rates up

July 26th, 2023: Rate hike, mortgage rates down

May 3rd, 2023: Rate hike, mortgage rates down

March 22nd, 2023: Rate hike, mortgage rates down

February 1st, 2023: Rate hike, mortgage rates down

December 14th, 2022: Rate hike, mortgage rates down

November 2nd, 2022: Rate hike, mortgage rates UP

September 21st, 2022: Rate hike, mortgage rates down

July 27th, 2022: Rate hike, mortgage rates down

June 15th, 2022: Rate hike, mortgage rates down

May 4th, 2022: Rate hike, mortgage rates down

March 16th, 2022: Rate hike, mortgage rates UP

I was curious what tends to happen with mortgage rates on Fed decision day so I looked at the past 12 decisions and used MND data for mortgage rate movement on the days in question.

I included the 11 rate hikes since March 2022 and the pivot to a cut yesterday. Unsurprisingly, as far as I’m concerned, mortgage rates tend to defy the Fed more often than not.

In other words, when the Fed raises rates, mortgage rates often fall. And when the Fed cuts, mortgage rates tend go up.

I’ll need more data on the latter piece as they continue to make expected cuts. But it wouldn’t surprise me to see this trend continue.

Just note that the mortgage rate movement post-Fed rate decision often isn’t significant. And over time, things can change a lot more.

For example, even though lenders often cut rates on Fed hike day, the longer-term direction of mortgage rates was decidedly higher.

Now we might see the opposite. As the Fed is expected to make additional cuts, lenders may gradually lower rates over time.

But again, it’s not because of the Fed! It’s the underlying data and direction of the economy.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 18 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on Twitter for hot takes.

{kind=link}